Imagine that you’re less than a month into retirement on a $5,000 per month fixed income and your water heater goes out. You’re facing a $5,000 bill for a replacement or you have to go without hot water. Without an emergency fund, you face a decision of accruing debt or dipping into your savings.

These unexpected expenses are more common than you might think— water heaters only last eight to 12 years and that’s just one of many possible large expenses. The good news is that you can prepare for these expenses in advance to eliminate stress and ensure that they don’t jeopardize your retirement nest egg.

Let’s take a look at a few unexpected retirement expenses that might crop up and how you can prepare for them.

#1. Medical Bills

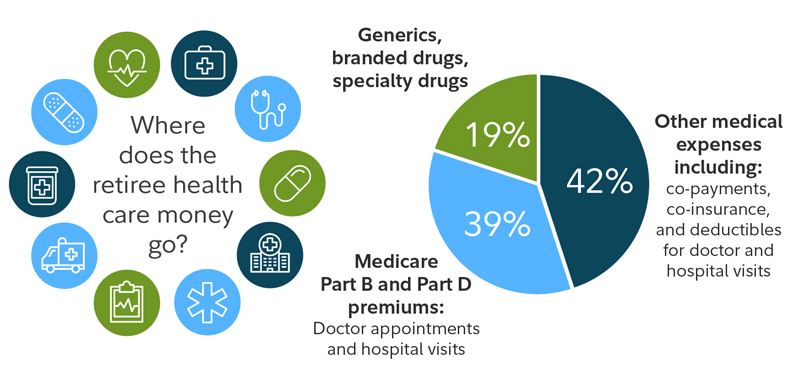

The average couple will need $285,000 in today’s dollars for medical expenses in retirement, excluding long-term care, according to Fidelity Benefits Consulting. These costs go towards co-payments, co-insurance, deductibles, doctor appointments, hospital visits and prescription drugs among other things.

Where do medical costs go? – Source: Fidelity

The best way to minimize these costs is to carry sufficient insurance. You should enroll in Medicare Parts A, B, and D when you’re first eligible to avoid a late-enrollment penalty and carefully consider the premiums, copays and different levels of supplemental insurance to find the right fit for you.

Prior to retirement, you may want to consider saving with a Health Savings Plan (HSA). These plans enable you to put away money before-tax that you can withdraw tax-free to cover qualified medical expenses. In addition, you aren’t taxed on any capital gains that accrue in these accounts over time. Keep in mind, you must have insurance coverage with a high deductible to be eligible to contribute to an HSA plan.

You should also consider long-term care insurance that covers nursing homes, assisted living, home modifications, care coordination and other medical service options. The cost of assisted living ranges from $2,000 to more than $6,000 per month—and it’s not covered by Medicare.

Thankfully, if you do experience a large medical bill, most places allow you to finance it at a low or zero interest rate. Don’t be afraid to ask for a payment plan or discount for paying immediately.

#2. Home Repairs

Most homeowners are familiar with replacing water heaters, paying for a new roof or experiencing any number of HVAC issues. While these events are stressful in the momentum, it’s even more stressful when you cannot afford a repair. You could be forced to take on expensive debt or sell assets.

The best way to minimize these costs is to save for them ahead of time. There are a couple of general rules that can help you determine how much to save:

- The 1% Rule: Save one percent of your home’s value every year for maintenance. For instance, if you have a $350,000 home, you should save $3,500 per year.

- The 10% Rule: Save ten percent of the total cost of your property taxes, mortgage and insurance payments. If you have a combined tax, mortgage and insurance payment of $1,500 per month, you should set aside $150 per month.

Unlike an HSA, it’s a good idea to keep these funds in a liquid account, such as a high-interest savings account that’s dedicated to home repairs (e.g. not a general account). You need to be able to quickly access the money if something happens without worrying about stock prices or capital gains.

Many retirees want to live in their homes as long as possible. That might mean making modification to make life easier. A ramp or bathroom improvement could make your home stay much safer or easier to live alone. It is best to make these changes before they are necessary so they don’t add unneeded stress.

#3. Death or Divorce

Divorces have decreased in nearly every age group, but they have been on the rise among those in retirement. So-called “grey divorces” have doubled since the 1990s as a new generation enters retirement. And, these divorces can be especially stressful when money is already tight.

While divorce isn’t something you can (or should) prepare for, you can take a few steps that would benefit your life with or without a divorce. The most important step that you can take is keeping all of your financial records organized and accessible to minimize a lawyer’s billable hours finding them.

The death of a spouse can be devastating and extremely stressful. Unlike a divorce, there are ways that you can plan ahead to remove financial stressors from the situation. First, discuss death with your spouse and how they will handle things when you are gone. Two other important steps are purchasing life insurance to cover costs and ensuring that you have an updated will.

#4. Children

Every parent knows that children are a common source of unplanned expenses—but few realize that it’s still true after they’re out of the house! So-called “boomerang children” may want to come live with you as adults when they’re between jobs or relationships, adding to your cost of living.

On the other end of the spectrum, you may be counting on your children to take care of you during retirement. If they don’t share your vision, you could be facing an unexpected decision to hire a live-in nurse or move to a retirement community—significant expenses for almost anyone’s retirement nest egg.

The best way to avoid these problems is to set expectations ahead of time. Tell your children that they will have to pay rent to stay with you as adults and ask them about their willingness to take care of you in retirement. These are uncertainties that can be eliminated with a conversation.

Build an Emergency Fund

These are only a handful of expenses that could put a strain on your retirement finances. For example, you could get into an accident with an uninsured motorist or have a pipe burst within your house. These costs can add up to thousands of dollars and quickly put a dent in your savings.

You can address any unexpected expenses by establishing a general emergency fund. While even $500 can save you from many financial scrapes, it’s a good idea to save up to a half year of your total expenses (e.g. electricity, insurance, mortgage, etc.) and put it into a dedicated savings account.

It might take a few years to build up to your target goal, but every dollar that you save along the way can help bail you out during an emergency and offset the amount that you’d need to take out of your retirement nest egg. The most important thing is getting started as early as possible.

The Bottom Line

There are many different types of unexpected retirement expenses, but you can plan for them in advance. From insurance policies to an emergency savings account, there are many ways to mitigate the impact of these one-time expenses on your fixed retirement budget and avoid dipping into your nest egg.

If you’re looking for ways to boost cash flow, the Snider Investment Method enables you to generate an income from your retirement stock portfolio. You can use this income to supplement your other retirement income or build up an emergency savings account.

Sign up to take our free e-course or learn about our managed options for a hands-off approach.