Most colleges provide a better return on investment than investing in the stock market, but at an average annual cost of between $10,230 for public universities and $35,830 for private universities (not including the cost of housing), it’s one of the most significant financial decisions that most people will make in their lifetimes.

One-third of students have a direct federal loan while national student loan debt topped $1.5 trillion in 2019. In combination with scholarships and grants, 529 Savings Plans can help you save for a child’s college education early on and reduce their need to turn to student loan debt. The flexible accounts can even help pay for primary and secondary school expenses.

Let’s take a look at how 529 savings plans work, pros and cons to keep in mind and other important considerations.

What Is a 529 Savings Plan?

The 529 Savings Plan is a tax-advantaged account designed to encourage saving for future education costs. All 50 states and the District of Columbia sponsor at least one type of 529 Savings Plan, but they are not necessarily guaranteed by the federal or state government. Private colleges and universities may also offer their own 529 savings plans.

There are two types of 529 plans:

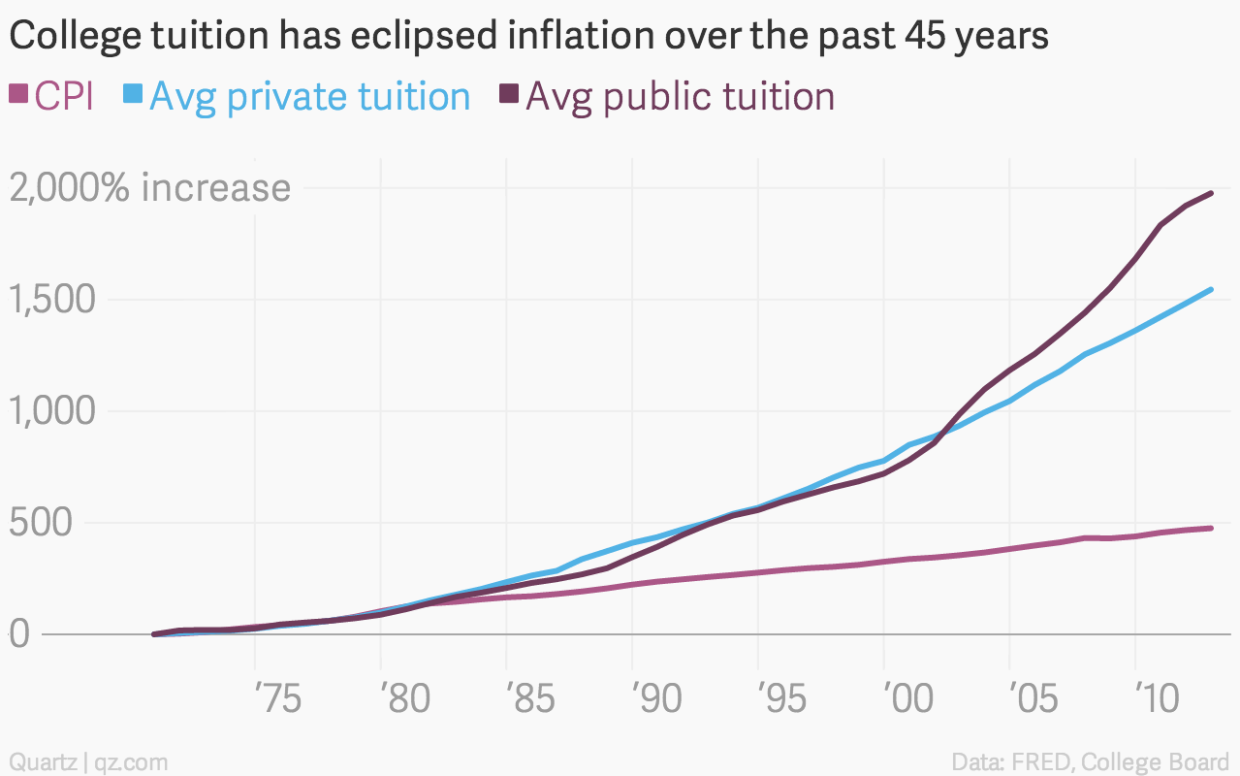

- Prepaid Tuition Plans: These plans let account holders purchase units or credits at participating colleges and universities (typically public and in-state) for future tuition and mandatory fees at current prices for a beneficiary. The cost of higher education has been increasing in price at rates much higher than inflation.

- Education Savings Plans: These plans let account holders invest in various funds and use the proceeds to pay for qualified educational expenses without paying taxes on the gains. It’s similar in many ways to a conventional retirement account.

As with most investments, those that start saving with a 529 plan early on realize the greatest benefit due to the impact of inflation and/or compounding interest. Many people choose to set up 529 accounts when their children are born and save a little over a long period of time to help mitigate the potential for a high lump sum cost in the future.

Pros and Cons to Keep in Mind

529 Savings Plans are a great way to save for a college education, but there are some important caveats, and they’re not right for everyone. You should carefully weigh the pros and cons before selecting 529 Savings Plans over the many alternatives to paying for a college education, such as using a taxable account or even student loans.

Pros

- Inflation: Tuition has risen at about twice the rate of inflation and prepaid tuition plans enable beneficiaries to avoid these rising costs by paying today’s rates. The plans could become an even better deal if higher education costs continue to rise.

- Tax: Qualified withdrawals from education savings plans are not subject to federal income tax, and in many cases, state income tax, making them an efficient way to save for the future — much like a ROTH IRA for retirement.

- Flexibility: Education savings plans can be used to cover a variety of education-related costs, including the cost of private primary and secondary school, as well as student housing and other education-related costs.

Cost of College Tuition vs. Inflation Over Time – Source: Quartz

Cons

- Penalties: Withdrawals from educational savings plans that are not related to education will incur state and federal income tax plus an additional 10% federal tax penalty — a hefty price to pay for the failure to use the funds for education!

- Risks: Many 529 Savings Plans are not guaranteed by the government, which means that a plan sponsor shortfall (e.g. a default due to a financial crisis) could result in losses that are never recouped by the account holder.

- Limitations: If a beneficiary of a prepaid tuition plan doesn’t attend a participating college, the plan may not cover the cost of education and only pay a small return on the original investment, making it a poor investment choice.

How to Open a 529 Savings Plan

Start by determining if a 529 Savings Plan is the right option for you. For example, you should always fund your own retirement before setting money aside for a child. You should also calculate how much money you need to save for a college education rather than saving an arbitrary amount, since saving too much money can have a high opportunity cost.

The next step is gathering all of your options. Using one of the many online tools available, you can narrow down all of the public and private options in your state. The right choice depends on the type of 529 plan that you want (prepaid tuition versus education savings plan) and the purpose of the account (funding private schooling versus saving for college).

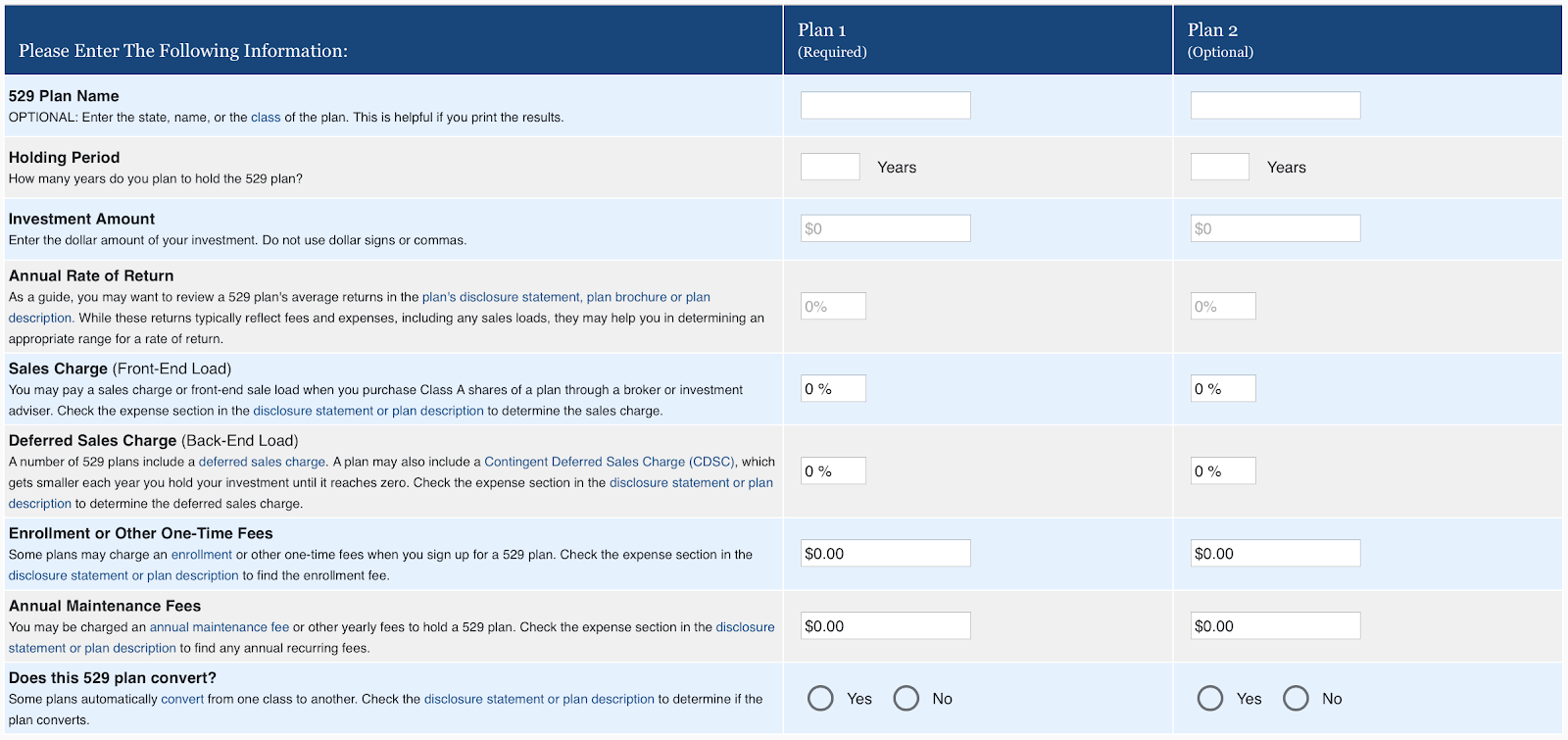

FINRA’s 529 Fee Analyzer Tool – Source: FINRA

You should carefully review the offering circular for each option to understand the fees and investment options. Using FINRA’s 529 Expense Analyzer, you can quickly compare fees and expenses that can reduce returns. You may also look at the fees associated with various fund options to see how those fees could impact the returns in your 529 account.

Important Tips to Remember

Most people assume that savings or loans are the only two ways to fund a college education, but there are many more resources available to make the costs more manageable. For instance, there are thousands of different scholarships and grants available for students of all types while advanced placement and community colleges can reduce required credits.

Popular ways to reduce the cost of college include:

- Scholarships and Grants

- Needs-based Financial Aid

- High School Advanced Placement

- Community College Credits

If you do choose a 529 Savings Plan, there are a couple tips that you can keep in mind to reduce costs:

- Direct-sold 529 plans from state governments often have lower fees than private 529 plans, so you should look at these options before other options if you’re open to your child attending a state school versus a private school.

- Large account balances, automatic contribution plans and other strategies may help reduce fees. While these discounts may appear small on the surface, they add up over time where the impact of compounding interest can be clearly seen.

You may also want to consult a financial advisor to help you analyze various options and make the best financial decision.

The Bottom Line

College is still a good financial decision for most people in terms of a return on investment, but the high cost forces many students to turn to loans. Parents that want to help out their children may want to consider 529 Savings Plans as a way to save for educational costs and help their children avoid student loan debt and the problems that come along with it.

If you’re looking for ways to save for retirement, Snider Advisors provides an easy-to-use method to generate an income using covered call options.

Sign up for our free e-course to learn more or contact us to learn about our managed services.