Many people are cynical when it comes to Social Security’s long-term viability. While news pundits may be quick to predict its imminent demise, a closer look at the program’s annual report shows that the most likely scenario is either a 25% cut in benefits or a 4.13% increase in payroll taxes—not a complete elimination of the program.

Let’s take a look at the state of the Social Security program, what you should count on in retirement and how to boost your retirement income without Social Security.

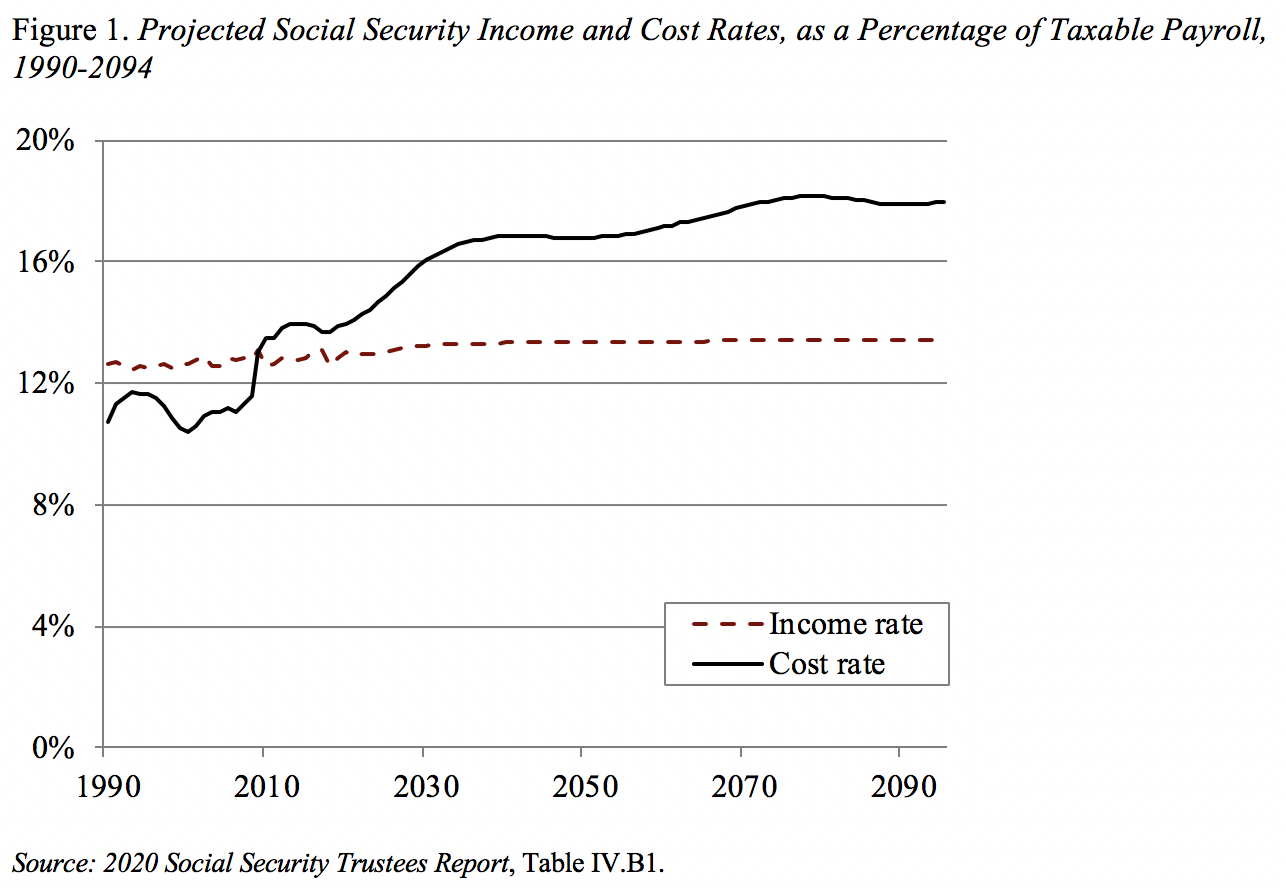

The Good News & the Bad News

The Social Security Administration recently released its 2020 Annual Report, providing key insights into the program’s sustainability and outlook over the coming decades.

The bad news is that the program’s costs (benefit payment outflows) have exceeded income (payroll tax inflows) since 2010. The annual report estimates that the program’s reserves will shrink from $2.9 trillion in 2020 to $1.8 trillion by 2029 before depleting entirely in 2034.

Social Security Costs Exceed Income – Source: 2020 SST Report

The Social Security Administration’s annual report was prepared prior to the COVID-19 outbreak, which is expected to have a modest impact on Social Security. For instance, if payroll taxes drop by 20% over two years, the depletion date could move up by about two years, which could be significant depending on your age.

The good news is that the reserve fund is only one source of income for Social Security. After the reserve fund is depleted, the program will still generate income from payroll taxes and taxing benefits. It’s highly unlikely that the entire program will collapse and pay nothing to retirees after 2034—it’s more likely that we will see a compromise.

The government outlines two options in the annual report:

- A permanent 4.13% increase in payroll taxes to 16.53% starting in 2035 would be enough to make the program sustainable at the current benefit level.

- A permanent 25% reduction in all benefits starting in 2035 would be enough to make the program sustainable at the current payroll tax level.

In short, the Social Security program isn’t all doom-and-gloom. Most people are likely to see at least 75% of their current estimated benefits upon retirement, while a decision to hike payroll taxes could ensure that the full amount remains in place.

How to Budget for Social Security

Most financial advisors recommend budgeting for conservative, but expected, outcomes. On one hand, you don’t want to save too much by assuming that Social Security will be gone by the time you retire. On the other hand, you don’t want to save too little by assuming that you’ll receive your full Social Security benefit throughout your retirement years.

As a general rule, you should assume that you will receive 75% of your estimated Social Security benefit, since that’s how much permanent funding is in place. You can see your estimated benefit by logging into your Social Security account or using their calculator to get a rougher estimate without having to create an account and sign in.

That said, it’s also a good idea to keep an eye on the Social Security Administration’s annual reports for any dramatic changes in estimates. Current or future administrations may decide to permanently cut payroll taxes to levels that would reduce the Social Security program’s income or expand Social Security benefits to create higher than expected outflows.

A holistic retirement plan should estimate how much you will require in retirement, calculate 75% of your Social Security benefit and invest enough to cover the remainder. If you’re not comfortable making these calculations on your own, it’s a good idea to seek the advice of a financial advisor.

Supplemental Retirement Income

Social Security income is great because it’s a check that you receive in the mail or via direct deposit each month. On the other hand, generating an income from investments often involves drawing down retirement portfolios—it can be a depressing process that can leave you feeling “poorer” over time as your portfolio depletes in value.

Fortunately, there are ways to generate retirement income from investments without reducing your principal investment. You can invest in a bond portfolio that pays a monthly or quarterly coupon, purchase certificates of deposit that guarantee payments or buy dividend stocks that pay a quarterly dividend—each without compromising the principal amount.

The Snider Investment Method is another option for generating an income from equities without being limited to dividend stocks. By writing call options against a portfolio of high-quality stocks, you can generate a monthly income without the need to sell stocks. You could even benefit from the long-term appreciation of stocks in your portfolio.

With the Lattco platform, Snider Investment Method users can easily identify covered call opportunities and maintain their own portfolio without paying professional management fees. You only need one day per month to make trades in just a few hours, leaving you with time to focus on enjoying your retirement years.

Sign up for our free e-course to learn more or contact us to learn about our asset management options.

The Bottom Line

Many people are cynical about Social Security, but in reality, you’re likely to receive most of your estimated benefit. While you shouldn’t count on a payroll tax increase to maintain 100% benefit levels, you can confidently assume that you’ll have at least 75% of your benefit at this point, while keeping an eye on any future developments.

If you’re looking for ways to boost your retirement income with less money coming in from Social Security, the Snider Investment Method may be right for you.