Covered calls are a popular way to generate an income from a portfolio of stocks, but you can also use them on exchange-traded funds (ETFs) and other securities. While the mechanics of setting up a covered call position are the same, there are some crucial differences between stocks and ETFs that you should keep in mind.

Let’s quickly recap how covered calls work and whether you should consider writing them against ETFs.

What Are Covered Calls?

Covered calls are options strategies whereby an investor sells the right to buy (call option) a long stock position they already own. For instance, suppose that you own 100 shares of Acme Co. You could establish a covered call position by selling one call option that gives the buyer the right to purchase those shares at a specific price before a certain date.

Most investors use call options to generate extra income from their portfolios. By giving up a little upside potential, they can reduce their cost basis and earn income above and beyond dividends. In some cases, investors use covered calls to generate an income to support their retirement without resorting to fixed-income investments.

Call option premiums depend on several factors, including:

- Strike Price – Call options with a strike price less than or close to the current price typically have higher premiums since there’s a good chance that the buyer could exercise the option.

- Implied Volatility – Volatile stocks typically have call options with higher premiums since there’s a higher likelihood that the stock moves enough to reach the strike price.

- Time Until Expiration – Call options with a long time until expiration trade at higher premiums since there’s more time for the underlying stock to move and reach the strike price.

Of course, selling high-premium options isn’t a guarantee of income. Covered call investors must balance these premiums against stock price declines, being called away, and on-going covered call management. For more information on building a complete strategy, Snider Advisors provides a series of free e-courses introducing you to portfolio management and other concepts.

Stock vs. ETF Covered Calls

Investors have access to more than 8,500 ETFs worldwide, including more than 2,600 in the United States. Surprisingly, these numbers aren’t that much higher than the total universe of U.S. stocks, which stands at around 6,000 companies and 8,000 ticker symbols. As a result, ETFs may offer investors more opportunities to profit from covered calls.

Despite the large number of ETFs, broad indexes have significantly less volatility than individual stocks (that’s kind of the point). And, of course, lower implied volatility translates to slimmer option premiums. As a result, ETFs generally have less income potential than individual stocks when it comes to executing covered call strategies.

That said, the lower income comes with less risk. You won’t experience any company specific risks when investing in an ETF. Losing a CEO, fraud, or lawsuits won’t impact an ETF’s price the same way they do on a company. ETFs are a great way to achieve diversification with one security. Sector, industry, or regional ETFs can offer great opportunities for covered call income without all the risks of owning an individual stock.

One note, we recommend our investors avoid both inverse and leveraged ETFs. These are more complex securities which require very close attention. In general, these securities aren’t meant to be long-term holds, which we believe is necessary when utilizing a successful covered call strategy.

ETF options may also fall under the 1256 contract rules, providing significant tax benefits. For example, some losses on a 1256 contract can be carried back, and you may be able to take a portion of short-term gains and convert them into long-term gains. However, not all ETF options fall under the 1256 (e.g., non-narrow-based security indexes).

Strategies for ETF Covered Calls

Covered call ETFs provide the easiest way to add options to your investment approach without writing the calls yourself. They write covered calls against benchmark ETFs, like the S&P 500, and. For example, the Global X S&P 500 Covered Call ETF buys stocks in the S&P 500 index and writes call options on the same index. In many ways, it’s similar to an S&P 500 SPDR ETF covered call strategy without having to manage options.You can find some of the top covered call ETFs here.

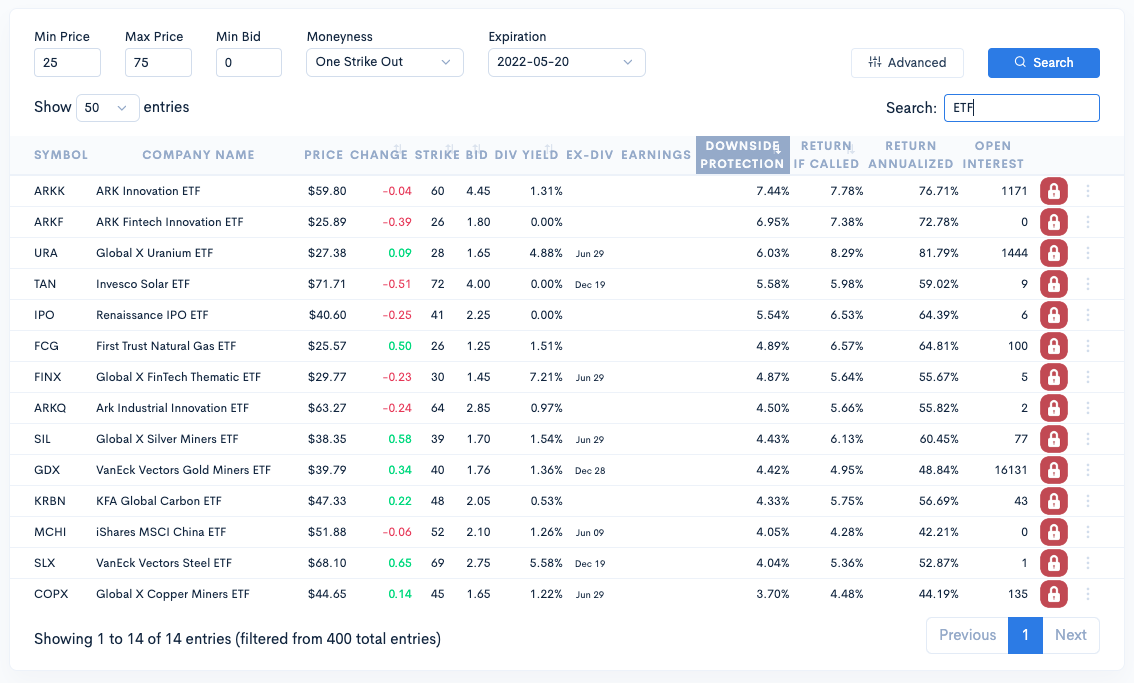

OptionDash makes it easy to find opportunities. Source: OptionDash

Investors that want the flexibility of managing their own covered call options can find opportunities using options screeners. For example, optionDash (pictured above) makes it easy to screen for covered call opportunities and sort them by annualized return, if-called return, downside protection, or other factors.

Snider Advisor’s Lattco trading platform also helps manage these opportunities after identifying them. The platform makes it easy to determine optimal asset allocations, manage positions over time, and see advanced reporting showing annualized returns and profitability. It goes hand-in-hand with the Snider Investment Method.

At Snider Advisors, our minimum investment is $25,000. Even at this level, the Snider Method and Lattco guide investors to use an ETF for their covered call portfolio. In our opinion, the lower risk of an ETF is more appropriate for these investors. As clients can create a diversified portfolio with additional assets, individual stocks makes more sense.

The Bottom Line

Covered calls are an excellent way to generate an income from a portfolio, but there are some caveats to keep in mind when using ETFs. For instance, ETFs may not offer as much income potential as stocks due to their lower levels of volatility, but they may provide tax advantages in a few cases where they’re not considered narrow-based indexes.

If you’re interested in trading covered calls, take our free e-course to understand how they work and develop an end-to-end strategy to manage trades. Or, inquire about our asset management services for a full-service option to generate income in retirement.