Investments for Inflation - Snider Advisors")

Inflation has become a substantial concern for investors over the past six months. Inflation now stands at 8.5% over the last 12 months,eroding the spending power of retirees. The sharp increase has been so dramatic that the Federal Reserve is likely to stop its bond-buying program early and raise interest rates for the first time since 2018.

Of course, inflation is generally negative for investment portfolios. For example, inflation reached an annual pace of about 9% between 1971 and 1981. As a result, the S&P 500’s real returns fell 16%, corporate bonds lost 23%, and Treasuries fell 38%. Many investors are concerned that today’s low Treasury yields could translate to similar losses.

Let’s look at the best and worst investments during inflationary periods and what that means for your portfolio.

A Historical Perspective

The 1970s provide a case study of the impact of inflation, but there are some critical caveats to keep in mind.

The top-performing asset class during the period was crude oil, but it would be a mistake to buy crude oil as an inflation hedge today. In the 1970s, a series of OPEC embargoes created a severe imbalance between supply and demand. These days, crude oil prices are on the rise due to supply disruptions, but not nearly at the scale of the 1970s.

Real estate investment trusts, or REITs, were another top-performing asset class in the 1970s. But, unlike the 1970s, the real estate industry already has the second-highest Shiller P/E ratio after Consumer Cyclicals at 60.1x, according to GuruFocus. These high valuations could limit upside and often translate to paltry dividend yields.

Finally, gold was another top-performing asset class during the 1970s. However, while gold tends to perform well during inflationary periods, the rise of inflation-protected securities (e.g., TIPS), cryptocurrencies, and other alternatives could make it less appealing to investors. As a result, its performance in the 1970s is hardly a guarantee for the future.

Inflation in Retirement

The best inflation strategy depends on your circumstances, risk tolerance, time horizon, and other requirements.

Retirement investors tend to be the most concerned with generating inflation-beating income. For example, if prices rise at 5% per year, a bond that pays 3% per year won’t cover your living expenses. At the same time, fixed-income investments (a staple of most retirement portfolios) tend to suffer the most during inflationary times.

Some alternatives to consider include:

- Series I Savings Bonds – These bonds pay a risk-free interest rate that adjusts to the consumer price index. These days, the bond has a risk-free yield of more than 7%making it an attractive way to generate risk-free income in an inflationary environment. You can learn more about these unique securities here.

- Covered Call Options – This strategy enables you to generate additional income from an existing stock portfolio by selling call options. That way, you can boost your income above and beyond dividend levels without turning to fixed income.

- Real Estate – Real estate remains a popular income producing asset. Most ‘hard assets’ tend to perform well in inflationary environments. More involved investors might consider acquiring a rental property to generate income and realize valuable tax write-offs.

If you want to use covered calls to generate income, the Snider Investment Method can help you select the right stocks and options to maximize your income. We help you generate consistent monthly cash flow in retirement from a portfolio of fundamentally-sound companies using a rules-based system to write covered calls.

Sign up for our free e-course to get started!

Inflation for Investors

Long-term investors are generally more interested in limiting their losses during inflationary periods.

The good news is that stocks tend to hold up better than bonds during these periods. For example, while the S&P 500 fell 16% between 1971 and 1981, the index outperformed bonds. Also, the decline wasn’t linear, meaning it would have been hard to time the market. For instance, the index fell about 30% in 1974, only to rise more than 30% in 1975.

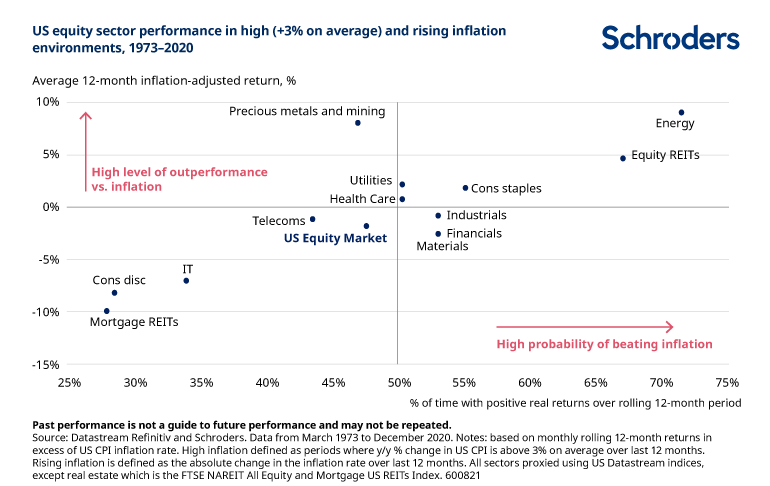

Sectors that perform best and worst during inflation. Source: Schroders

Long-term investors are better off subtly shifting their asset allocations during inflationary periods to limit losses. For example, in their equity portfolio, investors should allocate more to value stocks and less to growth stocks. In their bond portfolio, they should shift from long-term bonds to short-term bonds that are less sensitive to interest rate movements.

High net worth investors may also want to consider alternative investments for diversification. For instance, farmland, fine wine, artwork, and other markets provide a high level of diversification, mitigating the impact of inflationary periods. However, many of these assets are less liquid and more volatile than conventional stocks and bonds.

What You Should Avoid

The worst performing investments during inflationary environments are long-term fixed-income investments. After all, inflation leads to higher interest rates that hurt bond prices, and long-term bonds are locked into lower interest rates for an extended period. As a result, investors with a desire to hold fixed income should prefer short-duration bonds over long-duration bonds.

In the equity market, growth stocks tend to suffer during inflationary periods because they usually need to raise capital, and higher interest rates make that capital more expensive. The worst performing sectors are often technology, consumer discretionary, and telecoms, as well as mortgage REITs that are highly interest-rate sensitive.

The Bottom Line

Many investors are concerned about rising inflation. While gold and real estate provided an excellent hedge in the 1970s, today’s investors have many more options. Inflation-protected bonds, options strategies, and private real estate investments are all wonderful ways to boost income and protect your portfolio from the ravages of inflation.

If you’re interested in generating income while maintaining equity exposure, Snider Advisors can help you harness the power of covered calls and cash secured puts.

Sign up for our free e-course or inquire about our asset management services.