Most people save for retirement using a 401(k), pension or other employer-sponsored retirement accounts. If you don’t have that option, want to save extra or want more flexibility, individual retirement accounts, or IRAs, are a tax-efficient way to save for retirement.

If you already use a traditional IRA, you may want to convert it into a Roth IRA in order to realize certain tax advantages. For example, someone in between jobs for a year may want to take advantage of their low tax bracket to convert their savings to “after-tax” dollars.

Let’s take a look at Roth conversions, when it makes sense to do them and how to avoid common pitfalls in the process.

What Is a Roth Conversion?

Individual retirement accounts let you save money for retirement with certain tax advantages. Unlike an employer-sponsored plan, such as a 401(k), IRAs aren’t restricted to investments chosen by a plan sponsor and there aren’t any restrictions on the frequency of distributions. The fees on IRA investments may also be significantly lower than employer-sponsored plans.

The two most popular types of IRAs are:

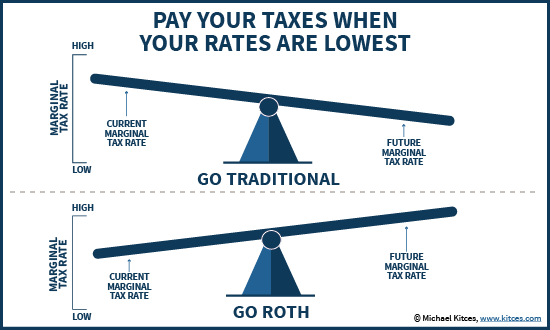

- Traditional IRA: You make contributions with money that you may be able to deduct on your tax return, and any earnings can potentially grow tax-deferred until you withdraw them at retirement. Since retirees tend to be in lower tax brackets than their pre-retirement selves, the tax deferral translates to lower tax rates.

- Roth IRA: You make contributions with money that you already paid taxes on, and any earnings can potentially grow tax-free with tax-free withdrawals in retirement, as long as certain conditions are met. The earlier that you start using a Roth IRA, the greater the tax benefit from tax-free earnings over time.

A Roth conversion involves taking all or part of the balance from a traditional IRA and moving it into a Roth IRA. For example, suppose that you want to convert a $100,000 traditional IRA into a Roth IRA. You would owe taxes on the $100,000 amount at the time of conversion in exchange for tax-free growth in the future, as long as you meet certain requirements.

Benefits of a Roth Conversion

Most people are aware of the tax benefits of a Roth IRA. Unlike other retirement vehicles, Roth IRAs enable you to avoid paying any taxes on withdrawals in the future—even if they double or triple in value before retirement. However, the tax savings is just one benefit of a Roth IRA that you should consider when determining if a conversion is right for you.

Roth vs. Traditional IRA – Source: Kitces

There are several reasons to consider a Roth conversion:

- Tax-free Retirement: You can withdraw money from a Roth IRA tax-free, as long as you meet certain requirements. By comparison, any withdrawals from a traditional IRA are subject to taxes on the earnings and the original contributions.

- No Required Distributions: You don’t have to take required minimum distributions, or RMDs, from a Roth IRA during your lifetime. By comparison, traditional IRAs have RMDs every year after you reach the age of 72, regardless of if you need the money.

- Tax-free Inheritance: Heirs must take RMDs from a Roth IRA, but they won’t have to pay federal income tax on the withdrawals if the account has been open for more than five years.

The biggest restriction on a Roth conversion is that there’s a five-year holding period before you’re able to make withdrawals. If you need the money in less than five years, you could owe tax on the withdrawal amount, which may defeat the purpose of the conversion. You should also keep in mind that the conversion involves a significant lump sum tax payment and increases your gross income, which can impact things like Social Security benefits.

How a Roth Conversion Works

The Roth conversion process involves a few simple steps. Before beginning the process, it’s a good idea to consider whether you want to stick with the same financial institution as the traditional IRA or consider a different institution. For example, some people choose to transfer to a brokerage that offers lower fees or commission-free trading.

One of the smartest reasons to do a Roth conversion is a back door conversion. High income earners aren’t able to contribute to Roth IRAs and their IRA contributions are not tax deductible. However, they can contribute to an IRA and immediately convert to a Roth. Since taxes were paid on the IRA contribution, no taxes are owed on the conversion. This works best when high income earners have no other retirement accounts. Conversions are done on a pro-rata basis. Other tax-deferred accounts limit the usefulness of a backdoor Roth conversion.

Once you make the conversion, you need to report the Roth conversion to the IRS using Form 8606 during the tax year that it takes place. You will also owe income tax on the tax-deductible contributions that you made into the account and the tax-deferred earnings that built up over the years, which can translate to a fairly large tax bill.

You may be tempted to use money from your traditional IRA to pay the tax bill for the Roth IRA conversion, but there are some important consequences to keep in mind before doing so. The money taken out will be considered a distribution and could result in an even higher tax rate if it pushes up your tax bracket and you lose out on the growth of that capital over time. It is also subject to an early withdrawal penalty if you are under the age of 59 1/2.

The Bottom Line

Roth IRA conversions are a good way to reduce taxes over the long-term, avoid RMDs, and leave tax-free money to heirs, but it’s important to keep in mind the near-term tax consequences of the move. Roth conversions make the most sense when you have a long time until you plan on taking distributions and/or anticipate being in a higher tax bracket.

If you’re looking for ways to boost your retirement income with a traditional IRA or Roth IRA, the Snider Investment Method leverages options to generate an income above and beyond dividend stocks and fixed income.

Take our free e-course to learn more or inquire about our asset management options.